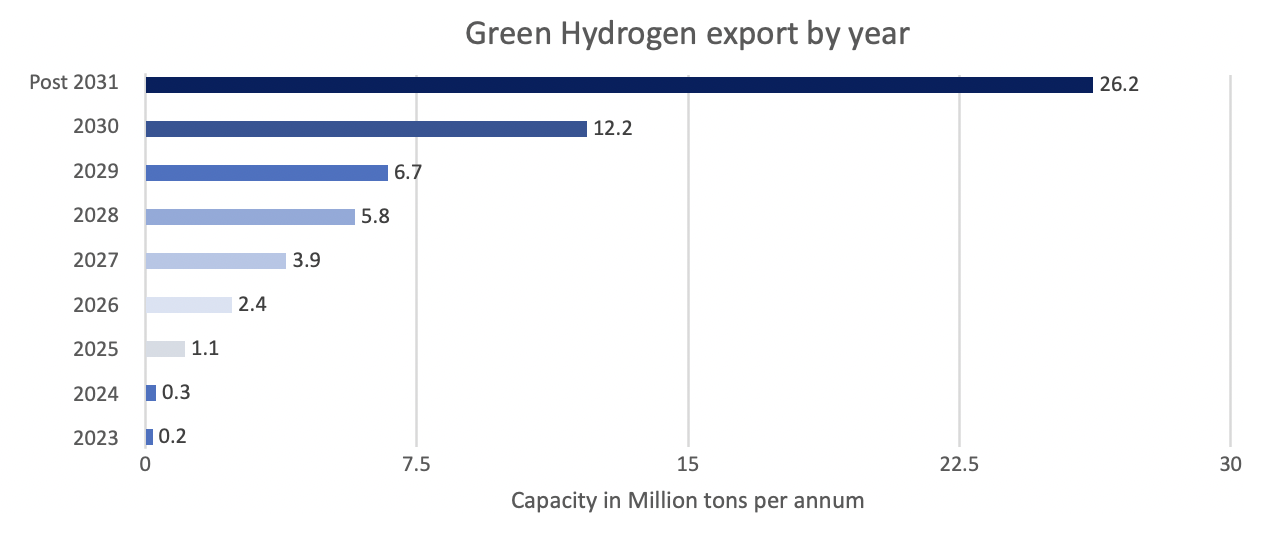

H2 Global foundation has launched the first tender for green hydrogen imports from outside EU. It will use double-auction program to buy green hydrogen or its derivatives from international producers through ten-year hydrogen purchase agreement (HPA). These derivatives can be shipped to the ports of Germany, Belgium and Netehrlands. ACE terminal and Cepsa sign agreement for green hydrogen and ammonia imports by creating supply chain from Spain to Netherlands Greenko to supply 250K tonnes green ammonia to Germany’s Uniper, 1st Indian co to start exports from 2025 VNG Handel & Vertrieb (H&V), the trading and sales subsidiary of VNG, and Total Eren’s cooperation will enable VNG to offtake the green ammonia on the German coast and make it available to its customers directly or in the form of hydrogen from 2028 onwards German utility company RWE has signed a Memorandum of Understanding (MoU) with Hyphen Hydrogen Energy to become the Namibian company’s preferred buyer of green ammonia for export to meet growing energy demand in Europe. RWE , LOTTE CHEMICAL Corporation (LOTTE) and Mitsubishi Corporation (MC) have formed a strategic alliance to jointly develop stable and large-scale clean ammonia (green and blue ammonia) supply chains in Asia, Europe and the US. Under the JSA, the partners agreed to jointly study the development of a large-scale ammonia facility that integrates green and blue ammonia production and leverages common infrastructure for international exports with a focus on Asia and Europe The Australian company Fortescue Future Industries (FFI) has signed a Memorandum of Understanding (MoU) with E.ON to deliver up to 5 Mt/year of green hydrogen to Europe by 2030, equal to around one-third of the calorific energy Germany imports from Russia. Yara and VNG: Ulf Heitmüller, CEO of VNG and Magnus Ankarstrand, President of Yara Clean Ammonia, signed an official cooperation agreement at the Yara plant in Poppendorf, near Rostock. It is a first step towards a future supply agreement between both parties and can eventually enable further projects to facilitate clean ammonia as a hydrogen and energy carrier into the German market, with Rostock as point of import. Hyphen has signed Memorandums of Understanding (MoUs) with a number of potential European customers, targeting the supply of up to 750,000 tonnes of green ammonia annually. The German government has decided to collaborate with the private sector on the construction of an import terminal for green ammonia in Hamburg. From 2026, the terminal will import green ammonia from Saudi Arabia. Air Products will produce the ammonia and distribute it to end users in Germany, mostly for conversion into hydrogen. Germany and Canada’s so-called 'Hydrogen Alliance' kicked off with the news that German utility Uniper has scooped an agreement to source 500,000 tonnes of green ammonia — made with renewable hydrogen — from a major new project on Canada’s Atlantic coast from 2025. In September 2022, Jera announced that it was working with ConocoPhillips and the German energy firm Uniper to develop a 2 million t per year clean ammonia plant on the Gulf Coast by the end of the decade. The partners intend to ship that ammonia to Europe. Japan’s IHI has signed a Memorandum of Understanding with India’s ACME Group - the developer of two large scale green hydrogen projects in Oman and Egypt- to explore offtake and investment opportunities in the former’s green hydrogen projects in Oman, India, USA and Egypt. Offtake contracts have also been signed between Saudi co-suppliers Ma’aden and Aramco and South Korea’s Lotte Fine Chemical, which will ensure that at least 50,000 tonnes of blue ammonia — derived from natural gas with carbon capture and usage — will be shipped from Saudi Arabia to South Korea. Supply contract has been signed for Japan’s Cosmo Oil to import an undisclosed amount of blue ammonia from Adnoc and Fertiglobe in Abu Dhabi. The largest of these deals has been struck between US ammonia trader Trammo and Canadian developer Teal for 800,000 tonnes of green ammonia (containing 141,000 tonnes of H2) produced via hydropower in Quebec, Canada. The second largest will see 100,000 tonnes of green ammonia (17,600 tonnes of H2) shipped by India’s Acme and Norway’s Scatec from Oman to Norwegian-headquartered ammonia player Yara International (the exact import country has not been specified). The Hydrogen Energy Supply Chain (HESC) project, Australia’s most advanced clean hydrogen project, has selected its preferred hydrogen provider and entered the commercial demonstration phase with a commitment from the Japanese Government’s Green Innovation Fund. An Australian joint venture between Japanese organizations, J-Power and Sumitomo Corporation (JPSC JV), has been selected as the preferred hydrogen provider to Japan Suiso Energy (JSE). The project will produce 30,000t of clean hydrogen gas per year in Gippsland, Victoria and JSE will liquify the hydrogen for export to Japan.